Table of Contents

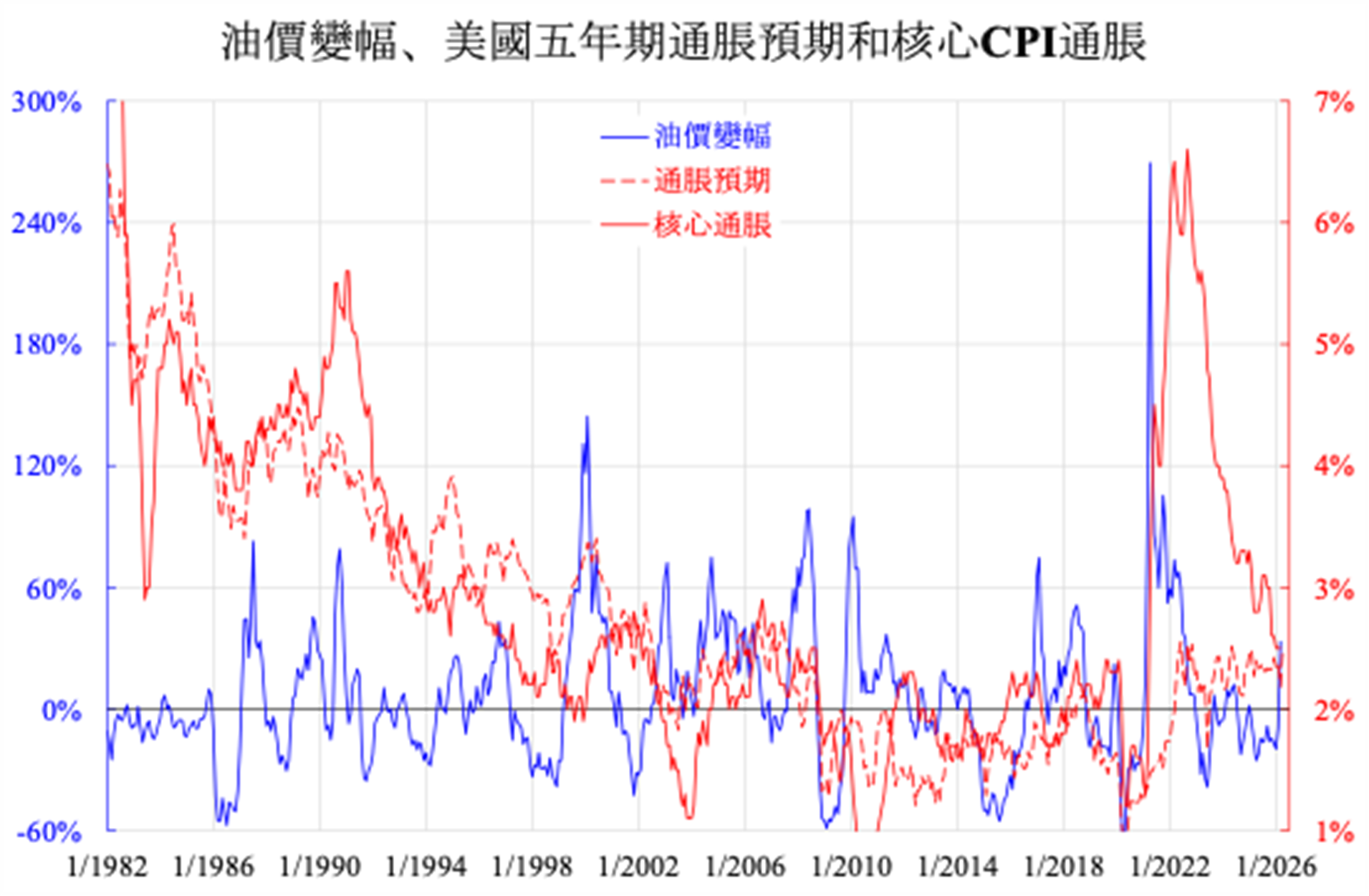

Oil prices have surpassed one hundred dollars a barrel, nearly double pre-war levels, and many anticipated a surge in inflation. What actually transpired was more modest: US headline CPI inflation rose from 2.4 per cent in February to 3.3 per cent in March, while core inflation edged up only marginally, from 2.5 per cent to 2.6 per cent. Four years ago, when oil hit 120 dollars, both headline and core inflation — already running high — barely moved further in the same two-month window. Can oil prices really drive inflation higher?

Since the stagflation era of the 1970s, oil price YoY change have tended to pull core inflation in the same direction, but by far less — typically no more than half a percentage point either way. The coincidence of 120-dollar oil and 9 per cent inflation during the Russia-Ukraine war has led many to assume intuitively that today's elevated prices will push inflation back toward those levels. Yet the two episodes unfolded against very different backdrops.

The previous oil price spike ran from early December 2021 to early March 2022, with prices climbing from 62 to 126 dollars. By late 2021, inflation was already running at 7 per cent; it reached 8.5 per cent by March 2022. Core inflation, however, rose only from 5.5 to 6.5 per cent over the same period. In practice, core inflation was close to peaking and did not continue climbing — a pattern quite unlike the 1970s. The explanation lies in inflation expectations.

The Federal Reserve's five-year inflation expectations measure has remained at or below 2.5 per cent for the better part of the past decade and a half, including four years ago. Had expectations been less well anchored, core inflation might well have converged toward headline levels. In 1980, when expectations became unmoored, the peaks for headline and core inflation were 14.8 per cent and 13.6 per cent respectively --- barely distinguishable. This illustrates how decisive inflation expectations can be.

The previous inflation surge actually began in March 2021, when prices started rising at a monthly pace of half to one percentage point. At that point, oil was still hovering around 60 dollars. The episode was driven not by oil but by the Fed's misjudged response to the pandemic supply shock --- deploying zero interest rates and quantitative easing when the problem was on the supply side. The subsequent oil spike the following year added comparatively little to inflationary pressure.

Monetary conditions today are neither tight nor particularly loose. With AI adoption advancing and the economic outlook subdued, both structural and cyclical forces are bearing down on inflation. Oil prices have already retreated sharply on ceasefire hopes. A repeat of 1980-style inflation looks unlikely. This is a case where history rhymes but does not repeat.