Table of Contents

Kevin Warsh is set to take over as Federal Reserve chair from mid-May, prompting scrutiny of how well he will withstand political pressure. In truth, today's environment differs markedly from the Nixon era: political interference is now conducted openly, requiring no investigative effort to uncover. Moreover, given the president's sweeping powers and the Fed's capacity to generate returns, any occupant of the White House has incentive to meddle — the only questions are of degree and visibility. The more pertinent issue is whether, under inevitable political pressure, the incoming chair can successfully guide the Fed towards its mandate of subduing both inflation and unemployment.

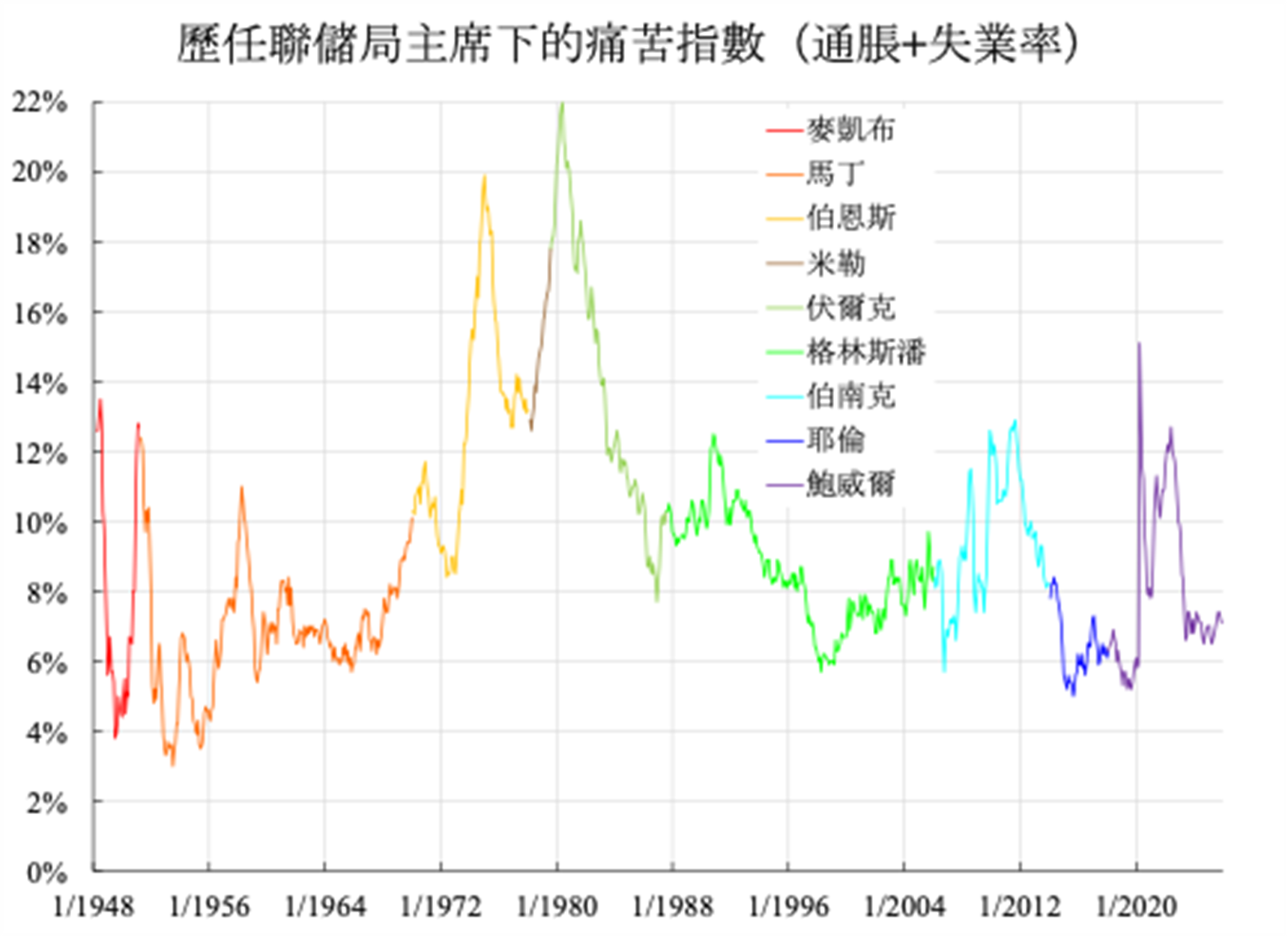

In practice, the Fed may weight inflation and employment differently, but both objectives carry equal statutory standing. A simple summation of the two — the Misery Index — therefore provides a useful gauge. The accompanying chart tracks performance under successive Fed chairs and should be interpreted as follows: cyclical fluctuations can largely be disregarded, but a sustained upward trend signals clear failure. During the stagflation era under Martin, Burns and Miller, the index climbed over two decades. By contrast, the roughly four decades since Greenspan have seen the index oscillate between 6 and 12 per cent, with no evidence of notably poor performance.

Historical experience suggests that absent persistent policy errors leading to stagflation, the Misery Index should spike to 8–9 per cent or above only in response to discrete shocks. Under normal conditions, it should range between 6 and 8 per cent, with inflation contributing 2–3 percentage points and unemployment 4–6 — levels that approximate equilibrium, or what markets term neutral and academics describe as optimal inflation and the natural rate of unemployment.

It bears noting that sustained rises in the Misery Index may not be attributable to any single chair, but rather to decade-long monetary accommodation driven by prevailing intellectual orthodoxy. Since the turn of the century, elements of this ideology have resurfaced — particularly after the financial crisis, when zero rates and quantitative easing became routine. Although the Misery Index over the past decade or so has appeared to fluctuate rather than trend, its amplitude has widened and skewed higher.

In other words, the legacy of the Keynesian revival this century may not be sustained stagflation, but more frequent episodes of transitory stagflation. Even if the median has shifted little while volatility has increased, the probability of losing control has risen — especially amid abundant liquidity, which heightens vulnerability to financial crises of various kinds.

{kind=link}