Table of Contents

Trump's policy actions immediately weaken the dollar. While this piece does not address currency markets per se, the proliferation of calls for de-dollarisation and US Treasury sales raises a pertinent question: do these reflect genuine structural weakness in America? A second question naturally follows: can foreign actors genuinely undermine America through de-dollarisation?

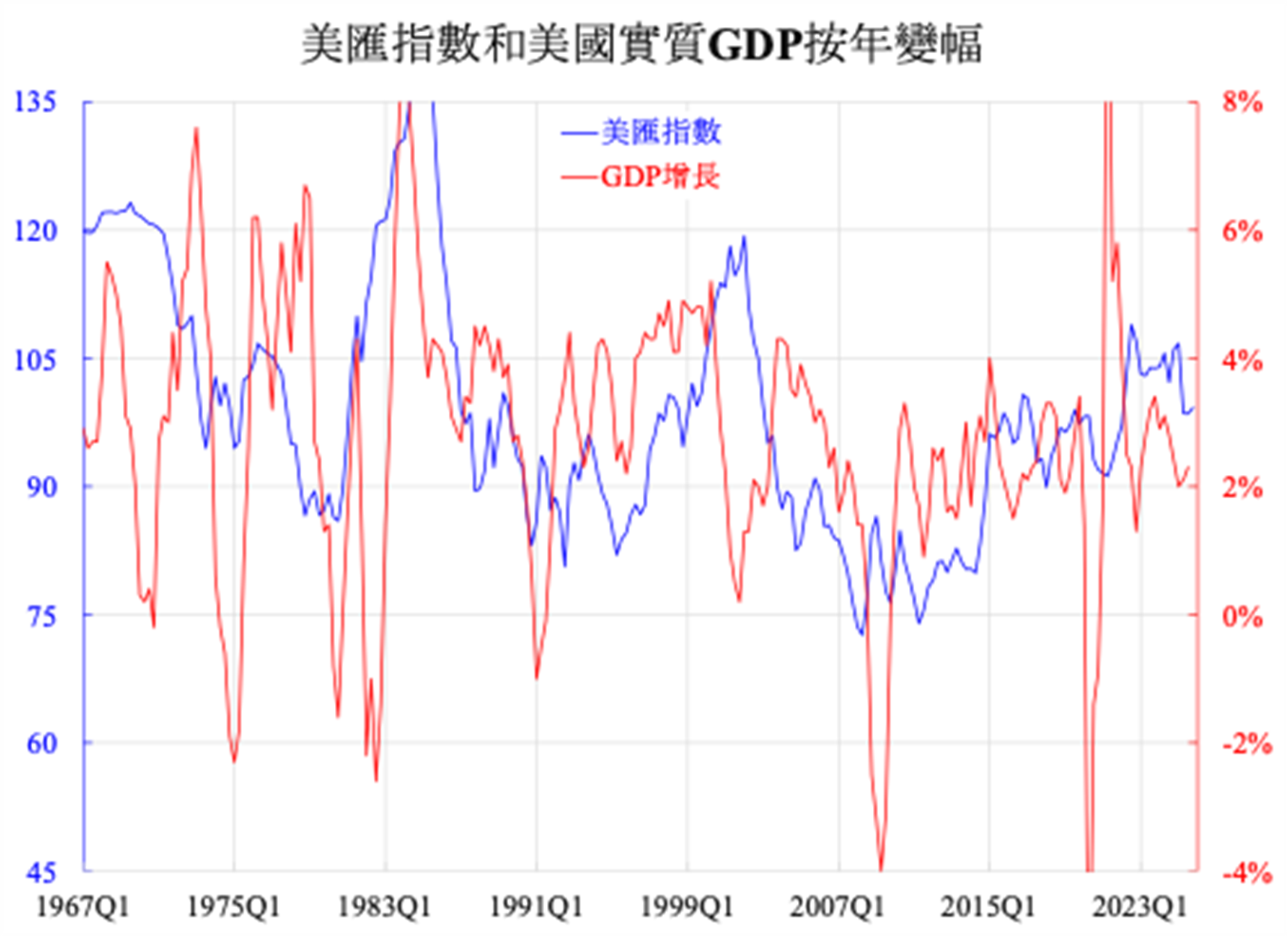

Empirically, the US Dollar Index clearly correlates with US GDP growth. As the accompanying chart demonstrates, this relationship is unmistakable, requiring no elaborate econometric modelling. Trump is surely aware of this correlation. Consequently, if he genuinely sought to weaken the dollar, he would either be consciously undermining American interests or would be perpetuating a false narrative—stating one thing while meaning another. Even if he truly desired depreciation, it would amount at most to a cyclical strategic manoeuvre, not a durable policy shift. Indeed, the moment foreign actors threaten to liquidate US Treasuries, or merely hint at doing so, Trump immediately capitulates—only to resume bluster thereafter.

Clearly, this positive correlation runs in both directions. As Tung Chee-hwa, the former Chief Executive of Hong Kong, once observed: when America prospers, the dollar strengthens; when the dollar strengthens, America benefits further. Generally speaking, exchange rates represent a nation's valuation. The proposition that a strong economy drives currency appreciation requires little elaboration. The reverse mechanism operates differently, however. Because the dollar functions as the global reserve currency, its exchange rate movements exert economic consequences extending far beyond the base-level dynamics of net exports.

The US Dollar Index has experienced cyclical fluctuations over the years, while the real broad effective Dollar Index has trended upward over the longer term. From this perspective, the dollar's position has at minimum remained intact, and arguably strengthened. As to whether foreign actors can weaken America through Treasury sales or currency manoeuvres, considerable obstacles emerge at the outset. Dollar-denominated assets command a dominant share of global holdings, particularly in large denominations. Sellers attempting to exit these positions struggle to reposition into equivalent alternative assets. Fundamentally, America has created such vast quantities of financial assets that de-dollarisation proves straightforward in theory but formidably difficult in execution. In essence, the dollar and the economy reinforce each other.

Today, currency deployment in financial markets has expanded substantially relative to currency usage in economic activity—encompassing trade, both domestic consumption and international commerce—compared to previous eras. In theory, Treasury positions and currency exposure could shift instantaneously into alternative monetary assets. However, as the foregoing analysis indicates, such transitions prove difficult in practice. Thus, while America's monetary hegemony may erode over time, it will not be swiftly displaced. American strength ultimately rests on institutional foundations. Its prosperity or decline does not depend on any single individual, including the presidency.